The Atom’s Promise: Why Nuclear Energy Still Divides the World

What if the most powerful energy source humanity has ever discovered is also the one we’ve consistently failed to master—not because of the physics, but because of the economics? Why do some countries build nuclear plants on time and on budget, while others seem trapped in a cycle of delays and cost overruns? And can a new generation of reactors—smaller, safer, smarter—finally deliver on nuclear’s original promise?

Welcome to FreeAstroScience.com. Today, we’re taking you on a journey through the real story of nuclear power: from its Cold War birth to the SMR revolution, from the shadow of Chernobyl to the bright hopes of fusion. We’re not here to sell you an ideology. We’re here to give you the numbers, the facts, and the honest scorecard—so you can decide for yourself.

This is a deep-dive reflection on nuclear power’s past failures, present reality, and future potential. We’ll show you why nuclear power costs so much, why some countries succeed where others fail, and what real innovation looks like in 2026. Stay with us to the end for a fuller understanding of one of the most consequential energy debates of our time. At FreeAstroScience, we believe that reason—not fear, not ideology—must guide our choices. Let’s keep our minds awake, because the sleep of reason breeds monsters.

From the Atom to the Grid — The Birth of Nuclear Power

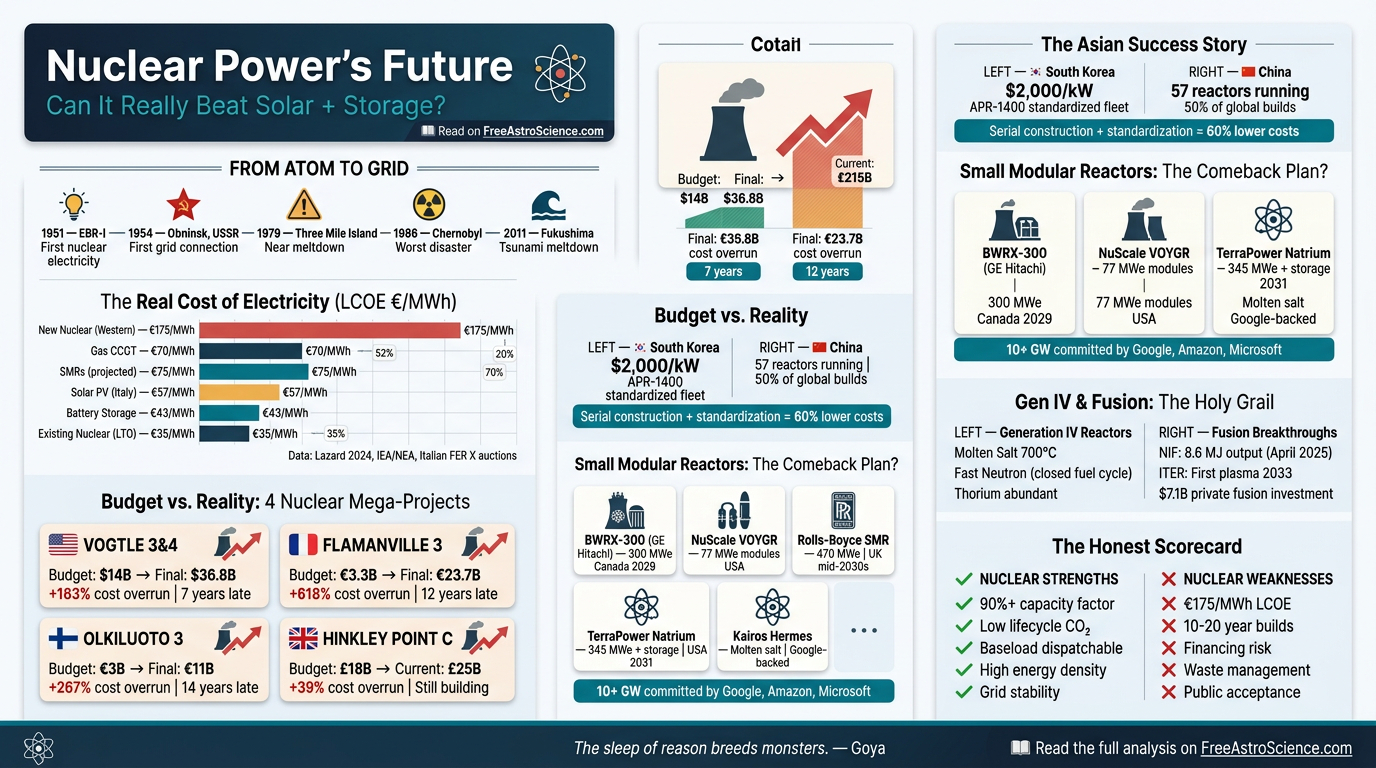

Let’s rewind to the early 1950s. The world was still reeling from the atomic bomb, but a new hope was rising: could we harness the atom for peace? In December 1951, the Experimental Breeder Reactor I (EBR-I) in Idaho lit up four light bulbs—the first electricity ever made from nuclear fission. It was a tiny start, but it changed everything.

Just three years later, the Soviet Union’s AM-1 reactor at Obninsk delivered 5 megawatts electric (MWe) to the grid. This wasn’t just a technical feat—it was a Cold War statement. The atom, once a weapon, was now a tool for progress. The United Kingdom followed with Calder Hall in 1956, firing up four 60 MWe reactors. The United States answered with Shippingport, Pennsylvania, in 1957—a 60 MWe pressurized water reactor (PWR) that ran until 1982.

The 1960s saw a flurry of innovation. Canada built the first CANDU reactor, using natural uranium and heavy water. France started with gas-graphite reactors but soon pivoted to standardized PWRs—a move that would pay off decades later. Japan and Germany joined the race, each eager to prove their technological prowess. Nuclear power wasn’t just about electrons; it was about national pride, scientific ambition, and the promise of a future where energy would never run out.

But let’s not kid ourselves. The early nuclear era was as much about politics as it was about physics. Every new reactor was a flag planted in the ground—a signal to rivals and allies alike. The atom’s promise was dazzling, but the risks were always lurking in the background.

The Golden Age and the Shadow of Three Disasters

By the 1970s, nuclear power was riding high. The oil crises of 1973 and 1979 sent shockwaves through the world economy. Suddenly, energy independence wasn’t just a slogan—it was a survival strategy. France went all-in, building a standardized fleet that would soon supply 70% of its electricity from nuclear. Globally, 20 to 30 new reactors came online every year in the late 1960s and 1970s. By the mid-1990s, nuclear power peaked at 17% of global electricity. The dream seemed within reach.

But then came the accidents. Three disasters—each different, each devastating in its own way—would change the course of nuclear history forever.

Three Mile Island, 1979 — A Near Miss That Changed Everything

March 28, 1979. Pennsylvania. At Three Mile Island Unit 2, a stuck valve, design flaws, and a string of operator errors led to a partial meltdown. The containment building did its job—no major radioactive release. But the damage was done. Public trust evaporated overnight. New reactor orders in the US stopped cold after 1978. Regulators clamped down, demanding more safety, more paperwork, more time. The golden age was over. Nuclear power would never be the same.

Chernobyl, 1986 — The Wound That Still Hasn’t Healed

April 26, 1986. Ukraine. A flawed safety test at Chernobyl’s Reactor 4 spiraled out of control. The reactor exploded, the core caught fire, and a radioactive cloud drifted across Europe. Thirty-one people died immediately, but the real toll was far higher—thousands of thyroid cancer cases in children, entire towns abandoned, a $200 billion economic scar that still hasn’t faded. The world watched in horror. The International Nuclear Event Scale was born. The IAEA rewrote its safety rules. But the trust was gone, and for many, it never came back.

Fukushima Daiichi, 2011 — The Wave That Reset the Debate

March 11, 2011. Japan. A magnitude-9 earthquake and tsunami overwhelmed the Fukushima Daiichi plant. Three reactor cores melted down. Over 150,000 people evacuated. The cost of decontamination? Between $470 and $660 billion. Germany shut down eight reactors on the spot and pledged to exit nuclear by 2022. Japan’s nuclear share crashed from nearly 30% to just 8.5% by 2023. Public opposition soared. Italy reaffirmed its anti-nuclear stance in a 2011 referendum. After Fukushima, only 22% of the global public considered nuclear “safe and important.” The debate was reset, and the future of nuclear power was thrown into doubt.

Why Is Nuclear Power So Expensive? The Real Economics

Let’s get real: nuclear power’s cost problem isn’t about the laws of physics. It’s about money, risk, and the brutal math of building something huge, complex, and rare. In the early 1960s, you could build a nuclear plant in the US for $1,500 per kilowatt (kW). By the mid-1970s, that number had jumped to $4,000/kW. Fast forward to 2024, and the US Energy Information Administration puts the overnight cost for a new plant at $7,821/kW. In Europe, it’s even higher.

The levelized cost of electricity (LCOE) tells the real story. Lazard’s 2024 analysis puts new US nuclear at $118–192 per megawatt-hour (MWh). Vogtle 3 and 4? $170–180/MWh. New European reactors? €165–175/MWh. Compare that to solar at €57/MWh in Italian auctions, battery storage at €43/MWh, and gas combined-cycle plants at $40–70/MWh. Nuclear’s LCOE is extremely sensitive to the discount rate: at 3%, it ranges from $27/MWh (Russia) to $61/MWh (Japan); at 10%, it jumps to $57–146/MWh. Stop construction for two years, and you add 15% to the final cost.

But here’s the twist: once a nuclear plant is running, fuel costs are low, and capacity factors are sky-high—often above 90%. Nuclear’s environmental externalities are tiny: 0.2–0.8¢/kWh, compared to coal’s 18¢/kWh. And nuclear provides baseload, dispatchable power—something intermittent renewables can’t do alone. The problem isn’t the physics. It’s the economics of building big, slow, and rarely.

| Technology | LCOE Range ($/MWh or €/MWh) |

Notes | Trend |

|---|---|---|---|

| New Nuclear (Western) | $118–192 / €165–175 | High capital cost, long build time, sensitive to discount rate | Rising |

| Solar PV (utility-scale) | €57 (Italy), $24–$60 (US) | Lowest cost in sunny regions, fast build, variable output | Falling |

| Onshore Wind | $26–$54 | Low cost, variable output, site-dependent | Falling |

| Battery Storage | €43 (Italy), $50–$80 | Enables renewables firming, short duration | Falling |

| Gas CCGT | $40–$70 | Low capital, fast build, CO₂ emissions | Stable/Volatile |

| Existing Nuclear (LTO) | $30–$40 | Life extension, very low cost, high reliability | Stable |

| SMRs (projected NOAK) | $60–$90 | Factory-built, modular, not yet proven at scale | Falling (if scaled) |

The Western Construction Disasters — A Pattern of Failure

Let’s talk about the elephant in the room: the West’s recent nuclear projects have been disasters—financially, logistically, and politically. Four projects stand out as cautionary tales.

Vogtle 3 & 4 (Georgia, USA) — The Most Expensive Power Plant Ever Built

Approved in 2009 with a $14 billion budget for two AP1000 reactors, Vogtle 3 and 4 were supposed to be online by 2016–2017. Instead, Unit 3 started in July 2023, Unit 4 in April 2024. The final bill? $36.8 billion. That’s $11,000–$16,000 per kW—by far the most expensive power plant ever built. Georgia ratepayers saw their electricity rates jump 24%. Vogtle’s LCOE is five times that of equivalent solar plus storage. Westinghouse, the reactor vendor, went bankrupt in 2017. Why? Construction started before the design was finished, supply chain failures hit 80%, electrician attrition hit 50%, and productivity was 13 times lower than expected.

Flamanville 3 (France) — 17 Years and Still Counting

Construction began in 2007 with a €3.3 billion budget and a 2012 target. The reactor finally connected to the grid in December 2024. The cost? €23.7 billion (about €21.1 billion in 2020 values). That’s €6,800–7,500 per kW. The problems? The design wasn’t finalized at the start, regulators changed the rules midstream, and a manufacturing defect in the reactor pressure vessel head forced a costly replacement.

Olkiluoto 3 (Finland) — Twenty Years for One Reactor

Olkiluoto 3 started construction in 2005 with a €3 billion budget and a 2009 target. It finally entered commercial operation in 2023. The final cost? Over €11 billion. Overnight cost: €5,310 per kW. This project became the poster child for first-of-a-kind (FOAK) risk—where every mistake is new, expensive, and hard to fix.

Hinkley Point C (UK) — Still Under Construction

Hinkley Point C was supposed to cost £18 billion. Now it’s over £23–25 billion ($32 billion), and it’s ten years behind schedule. The UK government guaranteed a strike price of £92.50/MWh (2012 prices, indexed to inflation) for 35 years—locking in high costs for decades.

| Project | Country | Start Year | Initial Budget | Final/Current Cost | Cost Overrun | Schedule Overrun | Notes |

|---|---|---|---|---|---|---|---|

| Vogtle 3 & 4 | USA | 2009 | $14B | $36.8B | +163% | 7–8 years | Most expensive plant ever; Westinghouse bankruptcy |

| Flamanville 3 | France | 2007 | €3.3B | €23.7B | +618% | 12 years | Design not finalized; vessel head defect |

| Olkiluoto 3 | Finland | 2005 | €3B | €11B | +267% | 14 years | FOAK risk; supply chain issues |

| Hinkley Point C | UK | 2016 | £18B | £23–25B | +39% | 10 years (est.) | Strike price lock-in; still under construction |

Why does this keep happening? It’s not just bad luck. Every new Western project faces a regulatory maze—unique licensing hurdles, $60 million in regulator fees per reactor, $180–240 million per design per country for vendor licensing. The supply chain has collapsed after decades of inactivity. The skilled workforce—engineers, welders, electricians—has retired or moved on. And then there are the “soft factors”: poor project definition, optimism bias, and strategic cost misrepresentation. Some projects underestimate costs by 50–100% just to get approved. The result? A cycle of disappointment and sticker shock.

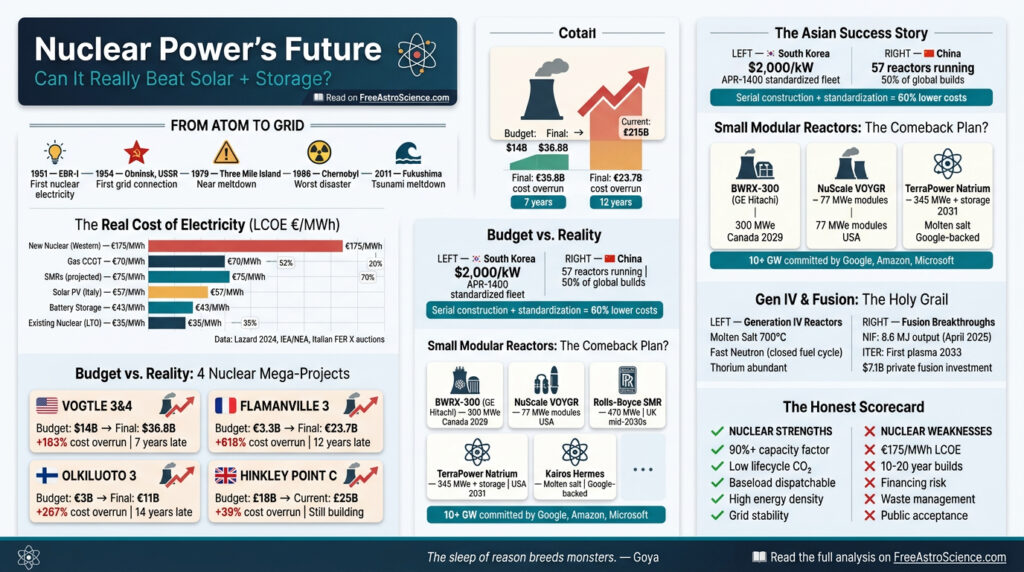

The Countries That Got It Right — South Korea and China

Not in Asia, though. South Korea and China have shown that nuclear power doesn’t have to be a financial disaster. South Korea’s overnight costs fell from $2,500/kW in the 1980s to $2,000/kW or less by the 2010s. How? Continuous construction, standardized APR-1400 designs, serial builds, and a vertically integrated supply chain. China now has 57 reactors operating and half of all reactors under construction globally. The IEA forecasts China’s nuclear capital costs at $2,500/kW by 2030 and $1,500/kW by 2050. Build two identical 1,000 MWe reactors on one site, and you cut costs by 15% per kW. China’s average CAPEX fell from €4,200/kW in 2015 to €2,800/kW in 2018, giving an LCOE of €67/MWh—the lowest among G20 countries with reliable data.

The lesson is simple: you can’t build cheaply if you build once every 20 years. Mastery requires repetition. If you want nuclear power to be affordable, you have to keep building, learning, and improving—just like any other industry.

Small Modular Reactors — Reinventing Nuclear from Scratch

So what’s the industry’s answer to the cost spiral? Modularity. Build smaller, in factories, in series. Small Modular Reactors (SMRs) are defined as reactors under 300 MWe, designed for factory fabrication, serial deployment, and enhanced passive safety. The hope is that by standardizing designs and building in bulk, we can finally break the cycle of cost overruns and delays.

GE Hitachi BWRX-300 — The Most Promising Bet in the West

Let’s start with the BWRX-300. This 300 MWe boiling water reactor uses passive safety—natural circulation and gravity, no active pumps or external electricity needed in emergencies. It’s a direct lesson from Fukushima. In April 2025, Ontario Power Generation received a construction license for the first BWRX-300 at Darlington, Canada. Target in-service: 2029. The full four-unit, 1.2 GW project is estimated at $15 billion. The Tennessee Valley Authority (TVA) also plans a unit at Clinch River, Tennessee, by 2032. This is the first real test of whether SMRs can deliver on their promise.

NuScale — The First, But Also a Warning

NuScale was the first SMR to receive US NRC design approval (50 MWe module, then uprated to 77 MWe in May 2025). The VOYGR plant can scale to 12 modules—924 MWe. But the flagship Idaho UAMPS project was canceled in 2023 due to rising costs and too few customers. Regulatory approval doesn’t guarantee commercial success. Still, NuScale’s partner ENTRA1 has a nonbinding agreement with TVA for up to 6 GW of capacity. The lesson? Even the best technology can stumble if the economics don’t work.

Rolls-Royce SMR — The Factory-Built Vision

Rolls-Royce’s SMR is a 470 MWe pressurized water reactor. The UK government has put up £280 million, matched by private investment, to build three dedicated factories for mass production. First deployment is targeted for the mid-2030s. If it works, this could be the model for affordable nuclear in Europe.

TerraPower Natrium — Generation IV Meets Grid Storage

TerraPower’s Natrium is a 345 MWe sodium-cooled fast reactor with integrated molten salt thermal storage. It can flex output up to 500 MWe for over five hours—essentially a nuclear-battery hybrid. The demonstration project broke ground in Kemmerer, Wyoming, in 2024. Projected cost: up to $4 billion, with half covered by the US Department of Energy. NRC’s final safety evaluation is expected by the end of 2025. Commercial operation is targeted for 2031.

Kairos Power Hermes — Molten Salt and Big Tech Money

Kairos Power’s Hermes is a 35 MWth fluoride salt-cooled reactor with TRISO fuel, under construction at Oak Ridge, Tennessee. NRC construction permit: late 2023. Expected operation: 2027. Google has partnered with Kairos for a fleet targeting 500 MW by 2030. Amazon and Microsoft are also anchoring SMR demand through power purchase agreements and investments. As of early 2026, over 10 GW in Big Tech SMR commitments exist. The future of nuclear may be written in code as much as in concrete.

| Project | Developer | Type | Size (MWe) | Location | Timeline | Status |

|---|---|---|---|---|---|---|

| BWRX-300 | GE Hitachi | Boiling Water Reactor | 300 | Canada, USA | 2025–2029 | Under construction |

| NuScale VOYGR | NuScale Power | Pressurized Water Reactor | 77 (module) | USA | 2023–2030s | First project canceled; new agreements pending |

| Rolls-Royce SMR | Rolls-Royce | Pressurized Water Reactor | 470 | UK | Mid-2030s | Pre-construction |

| Natrium | TerraPower | Sodium Fast Reactor + Storage | 345–500 | USA | 2024–2031 | Demo under construction |

| Hermes | Kairos Power | Molten Salt (FHR) | 35 (thermal) | USA | 2023–2027 | Demo under construction |

Generation IV — The Reactors That Could Solve Everything (If They Work)

Molten Salt Reactors — Running Hot and Waste-Free

Molten Salt Reactors (MSRs) operate at around 700°C and low pressure, making them inherently safer. China’s TMSR-LF1, a 2 MWt thorium prototype, reached full power in June 2024. In the US, Natura Resources is deploying MSR-1 in Texas by 2026. Terrestrial Energy’s IMSR targets the early 2030s. Mature MSRs could hit LCOEs of $60–80/MWh and can even consume existing nuclear waste. Deployment times are fast—just 3–4 years for some designs.

Fast Neutron Reactors — Closing the Fuel Cycle

Fast neutron reactors are the holy grail for nuclear waste. Russia’s BN-600 and BN-800 (1,480 MWe total) are operational. China’s CFR-600 (600 MWe) is running. TerraPower’s Natrium and Oklo’s Aurora are leading US projects. Russia’s BREST-OD-300, a lead-cooled fast reactor, will be operational in 2026. Fast reactors can use natural uranium and dramatically reduce the longevity of nuclear waste—a game-changer for waste management.

Thorium — The Abundant Alternative

Thorium is more abundant than uranium, produces less long-lived waste, and has a lower weaponization risk. China is investing billions in thorium MSR technology, aiming for a prototype by 2026 and commercial use by 2030. India’s 500 MWe Prototype Fast Breeder Reactor (PFBR) reached criticality in April 2026. The global thorium reactor market is projected to hit $9.06 billion by 2033, growing at 10.3% per year from 2026.

| Type | Coolant | Temperature | Key Advantage | Status |

|---|---|---|---|---|

| MSR | Molten Salt | ~700°C | Passive safety, waste burning, rapid deployment | Prototypes in China, US |

| SFR | Sodium | ~550°C | Closed fuel cycle, high efficiency | Operational in Russia, China |

| LFR | Lead | ~500°C | High safety, fuel flexibility | Demo in Russia (2026) |

| VHTR | Helium | ~1,000°C | Hydrogen production, high efficiency | Demo in China |

| SCWR | Water (supercritical) | ~600°C | High efficiency, simple design | R&D phase |

| GFR | Helium | ~850°C | High efficiency, fast spectrum | R&D phase |

Nuclear Fusion — The Holy Grail Is Closer Than We Think

Let’s be clear: fission splits atoms, fusion joins them. Fusion produces almost no long-lived radioactive waste and uses hydrogen isotopes as fuel—effectively inexhaustible. In December 2022, the US National Ignition Facility (NIF) achieved ignition for the first time: 3.15 MJ output from 2.05 MJ input. By April 2025, NIF hit 8.6 MJ from 2.08 MJ input.

ITER, the world’s largest tokamak, is under construction in France. It aims for 500 MW from 50 MW input (Q=10). The cost? €18–22 billion. First plasma is expected in 2033–34; deuterium-tritium operations in 2039. ITER won’t produce commercial electricity—it’s a demonstration machine.

Commonwealth Fusion Systems (CFS) is building the SPARC compact tokamak, targeting net energy demonstration and a 400 MW ARC pilot plant in Virginia by the early 2030s. They’ve raised $1.8 billion, with a $1 billion power offtake agreement with Italy’s Eni. Helion Energy’s 50 MW Orion plant aims to deliver electricity to Microsoft by 2028. Their Polaris prototype hit 150 million°C plasma in 2024. Private fusion investment has hit $7.1 billion globally by 2026. China leads public fusion investment at $1.5 billion per year—nearly double the US budget. The US DOE’s Milestone-Based Fusion Development Program expanded to $426 million in 2024.

Let’s be honest: commercial fusion power is still 10–20 years away. But it’s no longer just a pipe dream. The physics is proven. The engineering is catching up. The money is flowing. The holy grail is closer than we think.

Nuclear’s Role in the Energy Transition — Honest Scorecard

So where does nuclear fit in the energy transition? Here’s the honest scorecard. Nuclear’s strengths: baseload, dispatchable power; capacity factors above 90%; low lifecycle carbon emissions; external costs at 0.2–0.8¢/kWh (coal is 18¢/kWh); high energy density; grid stability. Weaknesses: high LCOE, long construction times, waste management, public acceptance, HALEU fuel supply chains, financing risk.

Thirty-eight countries signed the Declaration to Triple Nuclear Energy in December 2023, aiming to grow from 393 GWe in 2020 to 1,200 GWe by 2050. As of October 2025, there are 438 operable reactors worldwide (397 GWe), supplying about 9% of global electricity. Seventy reactors (78 GWe) are under construction, nearly half in China. The US Inflation Reduction Act provides $40 billion in loan guarantees and $700 million for HALEU fuel. The EU taxonomy recognizes nuclear as sustainable. Existing plants’ life extensions (LTO) are the most cost-effective nuclear option—LCOE often below $40/MWh.

In Italy, the government wants nuclear back. But the LCOE gap with renewables is real. Solar auctions clear at €57/MWh, battery storage at €43/MWh. Nuclear can help with grid stability and decarbonization, but only if we’re honest about the costs and the challenges. We can’t pretend the problem isn’t there—but we also can’t pretend nuclear has no role.

Conclusion

Nuclear power is one of/ humanity’s greatest engineering feats—and one of our most consistent economic disappointments, at least in the West, at least with big reactors. The accidents were real. The cost overruns were real. But so is the climate crisis, and so are the advances in SMR technology, Generation IV designs, and fusion research. We don’t need to be pro-nuclear or anti-nuclear. We need to be honest about what the data shows: cheap renewable energy with storage is already winning on cost, but nuclear’s reliability, density, and baseload power mean it still has a role—especially if SMR and Gen IV promises are delivered.

At FreeAstroScience, we explain complex science in plain terms. We believe that reason—not fear, not ideology—must guide our choices. As Goya warned, “The sleep of reason breeds monsters.” Let’s keep our minds awake. Come back to FreeAstroScience.com for more deep-dive science, and never stop questioning.

References

- World Nuclear Association — Economics of Nuclear Power ↗

- IEA — The Path to a New Era for Nuclear Energy (2023) ↗

- IEA/NEA — Projected Costs of Generating Electricity 2020 ↗

- World Nuclear Association — Nuclear Power in the World Today ↗

- IAEA — History of Nuclear Energy ↗

- Lazard LCOE Analysis v17 (2024) ↗

- Nature — Nuclear power after Chernobyl ↗

- GE Hitachi — BWRX-300 ↗

- ITER Organization ↗

- Commonwealth Fusion Systems ↗